On the 1st of March, South Africa based cryptocurrency exchange, VALR announced their $50M series B raise at a $240M valuation led by Pantera Capital. On that same day, Africa’s leading mobile operator MTN announced their purchase of 144 plots of virtual land in Africarare – the first African virtual reality metaverse featuring digital land. MTN is therefore the first African company in the metaverse. On 10th February 2022, the Central Bank of Kenya (CBK) issued a discussion paper on their Central Bank Digital Currency (CBDC), contrary to its previously held position that crypto was not allowed in the Kenyan banking industry. A day before the Central Bank of Kenya’s CBDC move, Zambia announced plans to complete research by the end of this year to create it’s CBDC. Africa’s cryptocurrency (crypto) market grew by 1,200% with $105.6 billion worth of crypto assets between July 2020 and June 2021, according to the 2021 geography of cryptocurrency report. A new African crypto exchange, www.topit.africa did $15 million in transactions in the last two quarters of 2021. In this concluding essay on Africa’s digital economy to end the first quarter, I focus on the emerging crypto economy in Africa.

CBDC is a digital currency issued by the central bank and intended to serve as legal tender while Crypto is a privately issued digital asset based on a network that is distributed across a large number of computers. The fundamental difference between CBDC and Crypto is the former is asset backed while the latter is not, so seeks to create value through some intrinsic mechanism like mining. One primary drawback is that the speculative nature of mining makes it considerably volatile. This has given rise to “stable coins” which are crypto asset that aim to maintain a stable value relative to a specified asset, or a pool of assets. A Global Stable Coin (GSC) is a stable coin with potential reach and adoption across multiple jurisdictions and could achieve substantial volume down the line.

On 25th October 2021, Nigeria became the first African country to launch its own CBDC by the Central Bank of Nigeria (CBN), about six months after the CBN issued a communique to banks to shut down customer accounts linked to crypto. At the launch, President Buhari said, “the adoption of a CBDC could improve economic activities and increase Nigerian GDP by $29 billion over the next 10 years.” In August 2021, the Bank of Ghana (BoG) announced a partnership with Giesecke+Devrient (G+D) to pilot a general-purpose Central Bank Digital Currency (retail CBDC) in Ghana. According to a 2021 survey of central banks conducted by the Bank for International Settlements (BIS), it was observed that 86% of central banks are actively researching the potential for CBDCs, 60% were experimenting with the technology and 14% were deploying pilot projects. In Africa, there are about a dozen countries exploring CBDCs according to a tracker by the Atlantic Council think tank.

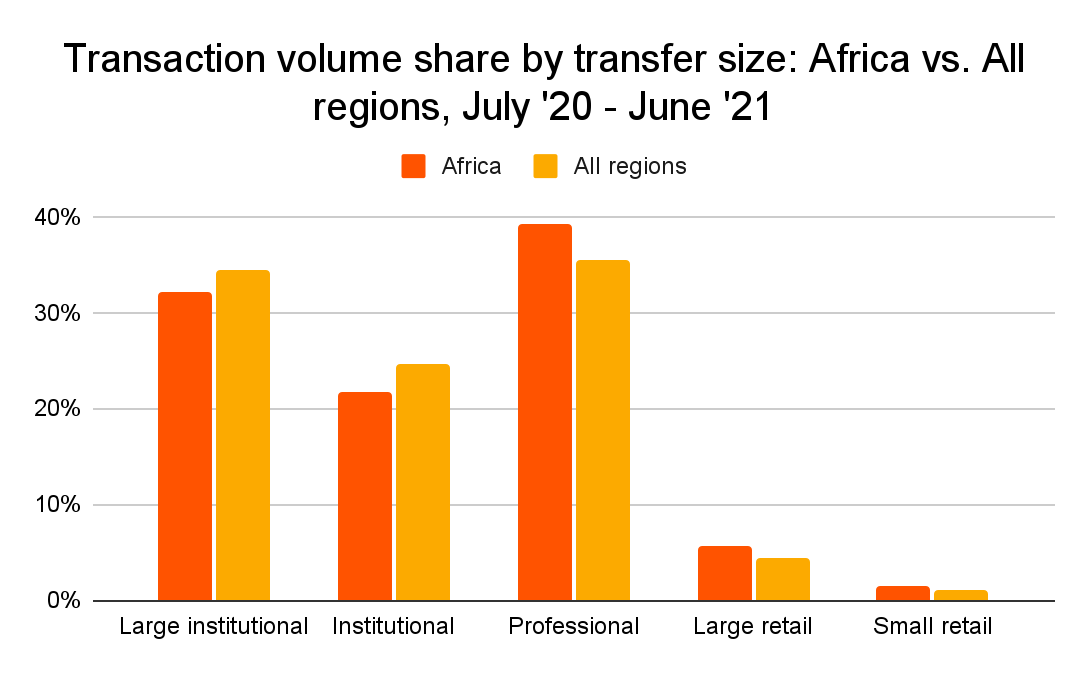

Even though Africa has the smallest crypto economy of any region, it has the highest grassroots adoption in the world with Kenya, Nigeria, South Africa and Tanzania all ranking in the top 20 of the Global Crypto Adoption Index. This has led to Africa having a bigger share of its overall transaction volume made up of retail-sized transfers than any other region at just over 7%, versus the global average of 5.5%. This is partly because crypto is reducing the high transaction cost in Africa when it comes to remittance and movement of money. Another reason for the adoption is the safeguard against inflation which keeps going up in most African economies.

And most importantly, it is a means of getting around regulations according to Edmund Higenbottam, managing director of Verdant Capital, who said that the popularity of the crypto currency was tied to the strict capital controls deployed on the continent. “Cryptocurrencies are a means of getting around regulation. And you see that in terms of the high usage of cryptocurrencies in countries that have very strong exchange controls or capital controls. You see using cryptocurrencies to get around regulation in many different ways, including money laundering regulations.” Nigerian Vice President Yemi Osinbajo said “Cryptocurrencies in the coming years will challenge traditional banking, including reserve banking, in ways that we cannot yet imagine. We need to be prepared for that seismic shift.”

Topsy Kola-Oyeneyin, Partner of McKinsey’s Payments Practice based in Nairobi, said “people look at crypto as a way of basically storing their money like a crypto stable coin, ready to be converted to the local currency as needed functioning as hedge against devaluation. They then realized that with the stored crypto, they can participate in crypto lending via a decentralized finance (defi) liquidity pool and earn some interest. So, all of a sudden your crypto actually becomes more valuable.” Then there are those who want a loan as the borrower so they can use their crypto assets as collateral for loans much faster than might be possible through traditional lending. This mimics the traditional savings and loans schemes that have been used in Africa for generations, now deployed using crypto. “It’s very exciting but there is still a gulf between the crypto opportunity and those who can access it. A number of the underbanked really don’t understand how to participate in the crypto market. That’s a challenge.”

That challenge seems to be less so in Sarafu, a network of community-governed digital currencies running on a public, non-profit university led decentralized ledger system called BloxBerg (an EVM Ethereum blockchain). Originally started in Kongowea village, Mombasa, spread to Nairobi’s slums and now in refugee camps such as Kakuma. It is cushioning these communities in the face of the corona recession as an alternative currency of settlement for the trade of community goods and services. The Sarafu’s community currency network has reported growth, totaling USD 3 million in trade for 58,600 users across Kenya. In Ghana, www.BenBen.com.gh is working with the Lands Commission and some banks to create a smart-contract based house financing system – these are the kinds of innovations that will bring the cyrpto economy to the mainstream in Africa in the not-too-distant future.